Look, we all saw this coming. When a company’s stock price is circling the drain, the old playbook gets dusted off. For Nakamoto, a company that’s apparently clinging to its 5,058 Bitcoin hoard like a life raft, that playbook involves a reverse stock split. Everyone expected something to happen after their latest earnings report landed with a thud, but nobody was betting on this particular maneuver. It’s a classic Silicon Valley-adjacent tactic, designed to make the numbers look less pathetic on paper, but does it actually fix anything? My money’s on ‘no’.

So, what exactly is happening here? The shareholders, bless their hearts, rubber-stamped a range for this reverse split – anywhere from a 1-for-20 to a grim 1-for-50. That means for every 20 to 50 shares you currently own, you’ll soon have just one. The idea? To push the per-share price up, making it look more substantial. It’s like putting on a tuxedo after you’ve lost all your money; it might fool some for a bit, but the underlying financial reality doesn’t change.

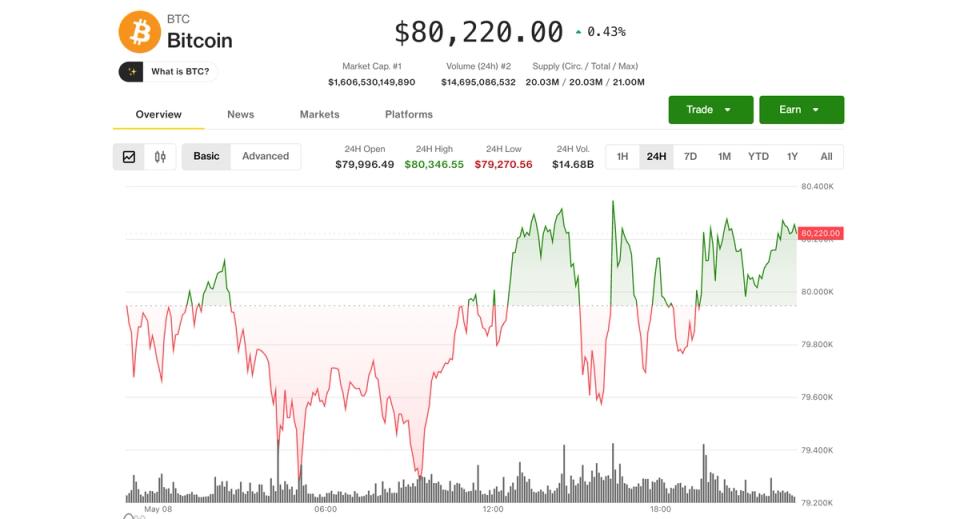

And let’s talk about that reality. Nakamoto dropped its first-quarter numbers last week, and while they crowed about a 500% quarter-over-quarter revenue increase – which sounds great until you see the details – they also posted a colossal $238.8 million net loss. A good chunk of that, over $102 million, was a “mark-to-market loss” on their Bitcoin holdings. The crypto dropped 23% that quarter, and Nakamoto’s treasury took the hit. Funny how that works when your primary asset is as volatile as a toddler on caffeine.

Who’s Actually Making Money Here?

This is the million-dollar question, isn’t it? Or in Nakamoto’s case, the several-hundred-million-dollar question. The company itself isn’t making money operationally; they even sold off 284 Bitcoin at the end of March just to cover basic expenses. So, who benefits from a higher share price? Primarily, the existing shareholders who don’t want their investment to look like pocket change. And perhaps the executives, whose compensation is often tied to stock performance, even if that performance is artificially boosted.

It’s a stark contrast to the early days of Bitcoin companies. Remember when the narrative was all about buying Bitcoin? Now, most treasury companies, with a few exceptions like Strategy and Metaplanet, have hit the brakes on acquisitions. Some are even liquidating their holdings to pay down debt, which is a sign of serious trouble. Genius Group, for instance, unloaded its entire 84 Bitcoin stash to keep the lights on. Nakamoto, meanwhile, is holding onto its treasury but simultaneously draining it for operational costs. It’s a balancing act that looks increasingly precarious.

Nakamoto’s current Bitcoin holdings place it as the 20th largest treasury company, just behind ProCap Financial. Michael Saylor’s Strategy still reigns supreme, dwarfing everyone else with over 843,000 BTC. But having Bitcoin doesn’t automatically mean you’re doing well. It just means you have a lot of a very volatile asset. And when that asset tanks, as it did this past quarter, your company’s financial health tanks with it.

The company announced its first-quarter financial results on May 14, recording a 500% quarter-over-quarter increase in revenue but a $238.8 million net loss, with more than $102 million attributed to a mark-to-market loss on its 5,058 Bitcoin (BTC) treasury after the cryptocurrency fell 23% during the quarter.

This reverse split is less about strategic growth and more about cosmetic surgery for the balance sheet. It’s a move designed to avoid delisting from exchanges and perhaps attract institutional investors who shy away from penny stocks. But it doesn’t address the fundamental issue: Nakamoto’s profitability, or lack thereof, and its heavy reliance on the capricious winds of the Bitcoin market. Are they trying to save the company, or just delay the inevitable reckoning? The cynicism is practically dripping from the press release.

What’s the historical parallel here? Think of any company that, faced with dwindling market value and revenue struggles, resorted to financial engineering. It’s a tactic often employed when the underlying business isn’t performing. It’s a smoke-and-mirrors approach that can buy time but rarely solves the core problems. If the Bitcoin price doesn’t surge dramatically, and if Nakamoto can’t find a sustainable way to generate revenue beyond selling its precious BTC, this reverse split will be nothing more than a temporary band-aid on a gaping wound.

Why Does This Matter for Bitcoin Treasuries?

This move by Nakamoto highlights a growing pressure point for companies holding significant Bitcoin reserves. The allure of Bitcoin as a treasury asset is its potential for appreciation, but its volatility is a double-edged sword. When prices drop, as they did this past quarter, these companies face significant paper losses that can impact their stock price and investor confidence. It forces a difficult choice: sell Bitcoin to cover expenses and reduce exposure, or hold on and risk deeper losses. Many are finding that a pure buy-and-hold strategy for treasury purposes, without a clear path to operational profitability, is becoming increasingly untenable in the face of market downturns.

🧬 Related Insights

- Read more: Figure’s Crypto Loans: Democratizing Collateralized Debt?

- Read more: Bitcoin Shrugs Off U.S.-Iran Talks—Is Crypto Asleep at the Wheel?

Frequently Asked Questions

What is a reverse stock split? A reverse stock split is a corporate action in which a company reduces the number of its outstanding shares, usually by consolidating them. This increases the per-share market price, making the stock appear more substantial and potentially meeting exchange listing requirements. It does not change the company’s overall market capitalization or the total value of an investor’s holdings.

Will this reverse split save Nakamoto? It’s unlikely to be a long-term solution. While a reverse split can temporarily boost a share price and prevent delisting, it doesn’t address Nakamoto’s underlying financial performance or its reliance on Bitcoin price fluctuations. Without improved operational revenue or a sustained Bitcoin bull market, the company could still face significant challenges.

Has Nakamoto sold Bitcoin recently? Yes. Nakamoto sold 284 Bitcoin on March 31 to cover operational expenses, and it did not purchase any Bitcoin during the first quarter of the year.