Banking goes agentic.

That’s the audacious claim coming from Anchorage, a digital asset bank that’s not just dipping its toes into the AI-powered financial future, but aiming to build the very foundations for it. This isn’t about chatbots answering your queries or algorithms trading stocks; we’re talking about autonomous entities, AI agents, performing financial transactions—paying each other, paying merchants, and even getting paid themselves. Nathan McCauley, Anchorage’s CEO, speaking at Consensus 2026, threw down the gauntlet, predicting a “trillion-dollar industry” built on this nascent concept. It’s a bold vision, one that’s already echoing across the fintech and crypto landscape.

So, what exactly is agentic banking? Think of it as delegating complex financial workflows to AI. Instead of you manually initiating a payment for a software subscription, an AI agent could be programmed to monitor your usage, determine the payment amount, and execute it autonomously, drawing from a pre-funded digital wallet. This requires not just sophisticated AI but also secure, programmable financial infrastructure capable of handling these automated, high-frequency interactions. Anchorage’s play here is to be the regulated bank that provides that secure, compliant plumbing.

Is This Just Crypto Fantasyland?

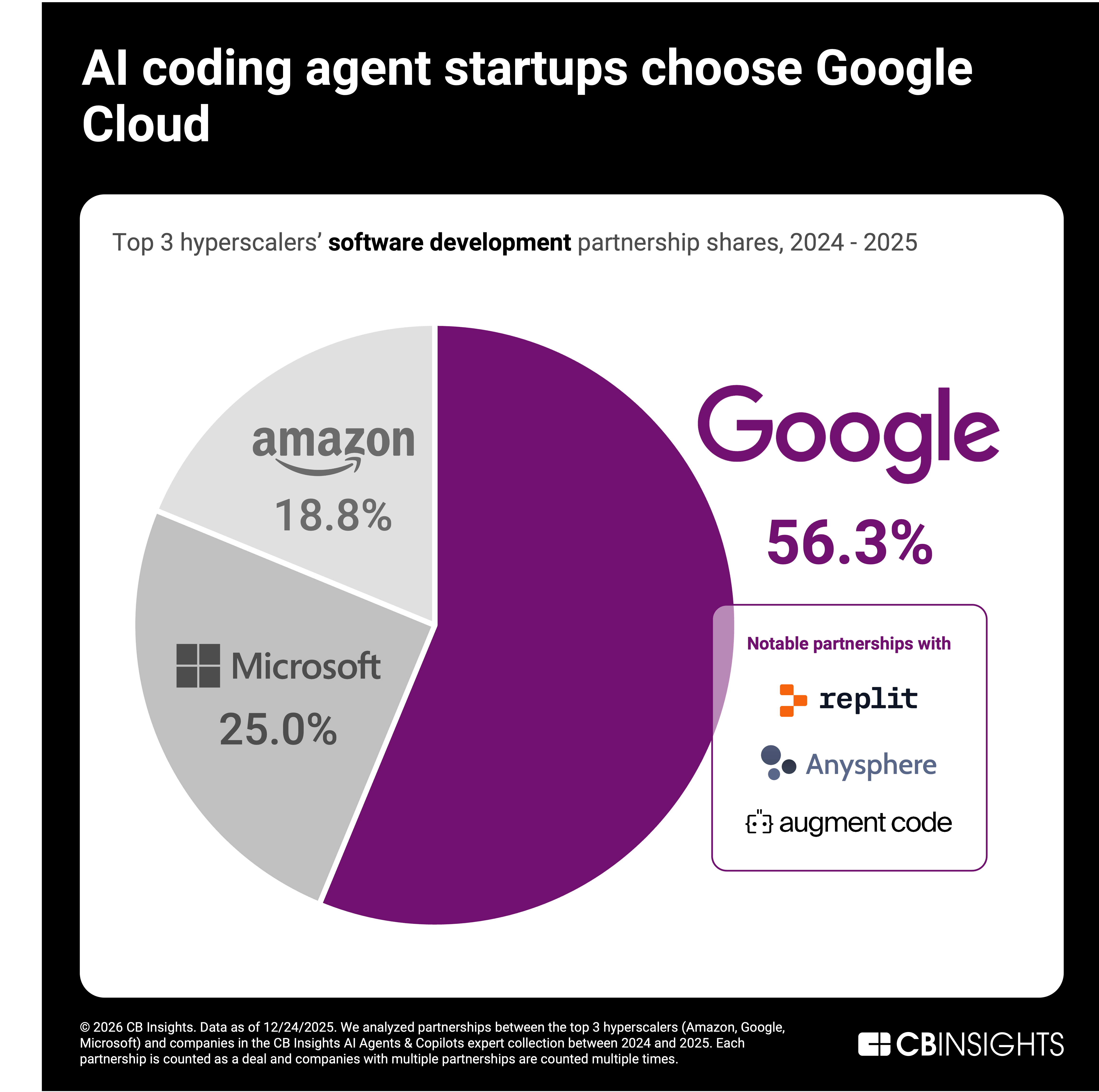

It’s easy to dismiss McCauley’s prediction as the usual Silicon Valley hyperbole. But look closer at the surrounding market signals. The trend Oliver Segovia, a Ripple Labs researcher, pointed out—the deepening collaboration between tech labs and regulated banks—is already in motion. Hyperscalers, once just service providers, are now exploring deeper integration into regulated financial systems, while banks are increasingly looking to build AI-driven intelligence on top of their existing core infrastructure. This symbiosis is precisely what enables agentic finance to move from theoretical discussions to tangible products.

We’re already seeing early iterations. Just days before McCauley’s pronouncements, the Solana Foundation partnered with Google Cloud to enable AI agents to pay for APIs using stablecoins on Solana. Then there’s Oobit, a crypto wallet startup backed by Tether, which launched a Visa-supported virtual card that allows AI agents to make online purchases using USDT. The kicker? These cards are funded directly from Tether’s treasury, eliminating the need for intermediaries and complex fiat on-ramps for the agents. This de-risks and streamlines the entire process, making autonomous transactions far more feasible.

“This is, in my view, set to be a trillion-dollar industry where we are going to have agents paying each other, agents paying merchants, and agents getting paid.”

This isn’t just about crypto, though. The underlying architecture being built—programmable money, secure digital asset custody, and automated compliance—has broader implications. Anchorage, as a regulated bank, is attempting to bridge the gap between the wild west of decentralized innovation and the established, secure world of traditional finance. Their bet is that the future of financial transactions will be increasingly automated and intelligent, requiring a trusted intermediary that understands both the regulatory landscape and the technical intricacies of digital assets and AI.

The Architectural Shift: From Humans to Agents

The fundamental shift here is from human-centric to agent-centric financial operations. For decades, banking infrastructure has been built around the assumption that a human will be initiating, approving, and monitoring every transaction. Agentic banking requires a complete rethink. We need systems that can:

- Execute autonomously: Without human intervention.

- Comply automatically: Ensure transactions adhere to regulations in real-time.

- Reconcile smoothly: Track and record complex agent-driven flows.

- Scale infinitely: Handle the sheer volume of potential AI transactions.

Anchorage’s positioning as a regulated bank is its key differentiator. While other players are building decentralized protocols or wallet solutions, Anchorage aims to provide the foundational, compliant layer that larger institutions might eventually plug into. This isn’t just about offering a new product; it’s about building the infrastructure for the next generation of financial activity, where AI agents become primary economic actors.

There’s a historical parallel to be drawn here. Think back to the early days of the internet. Companies that built the secure, reliable infrastructure for online transactions—the payment gateways, the hosting services, the secure protocols—ended up capturing immense value, even if they weren’t the ones building the end-user applications. Anchorage is making a similar play in the agentic finance space.

However, the path forward is fraught with challenges. Regulatory clarity will be paramount. How do you assign liability when an AI agent makes a fraudulent transaction? What are the capital requirements for entities facilitating these automated flows? These are not minor details; they are existential questions for an industry that, by definition, operates outside traditional human oversight for many of its core functions. The risk of AI-driven hacks, as highlighted by some in the DeFi community, is also a tangible threat that necessitates incredibly strong security and detection mechanisms. Anchorage’s deep roots in compliance might be its saving grace, or it could be the very thing that slows it down.

Ultimately, the success of agentic banking hinges on its ability to demonstrate tangible value and build trust. If Anchorage can indeed provide a secure, compliant, and scalable platform for AI agents to transact, McCauley’s trillion-dollar prediction might just be a conservative estimate. It represents a fundamental re-architecting of how value moves, driven not by human desire, but by algorithmic necessity.