Agents can now pay. Yes, you read that right. For two decades, I’ve watched Silicon Valley churn out shiny new objects, each promising to reinvent… well, everything. And here we are, talking about giving our digital sidekicks the keys to the digital kingdom, or at least, the digital credit card. Link and Stripe have rolled out what they’re calling ‘Link’s wallet for agents,’ built on Stripe’s ‘Issuing for agents’ platform. The pitch? Empowering AI agents to participate in the internet economy. Translation: letting your personal AI assistant actually buy things for you online.

It sounds futuristic, and frankly, a little terrifying. We’ve spent years marveling at how capable AI has become, with models spitting out code, writing essays, and even crafting passable poetry. But the real-world friction? Making purchases. Most payment protocols are still living in the past, clinging to the archaic systems that you and I use every day. So, the grand solution? Give these agents their own virtual cards or Shared Payment Tokens (SPTs), tied to your existing payment methods, without ever exposing your actual card details. Sounds clean. Sounds… like another layer of abstraction designed to make someone rich.

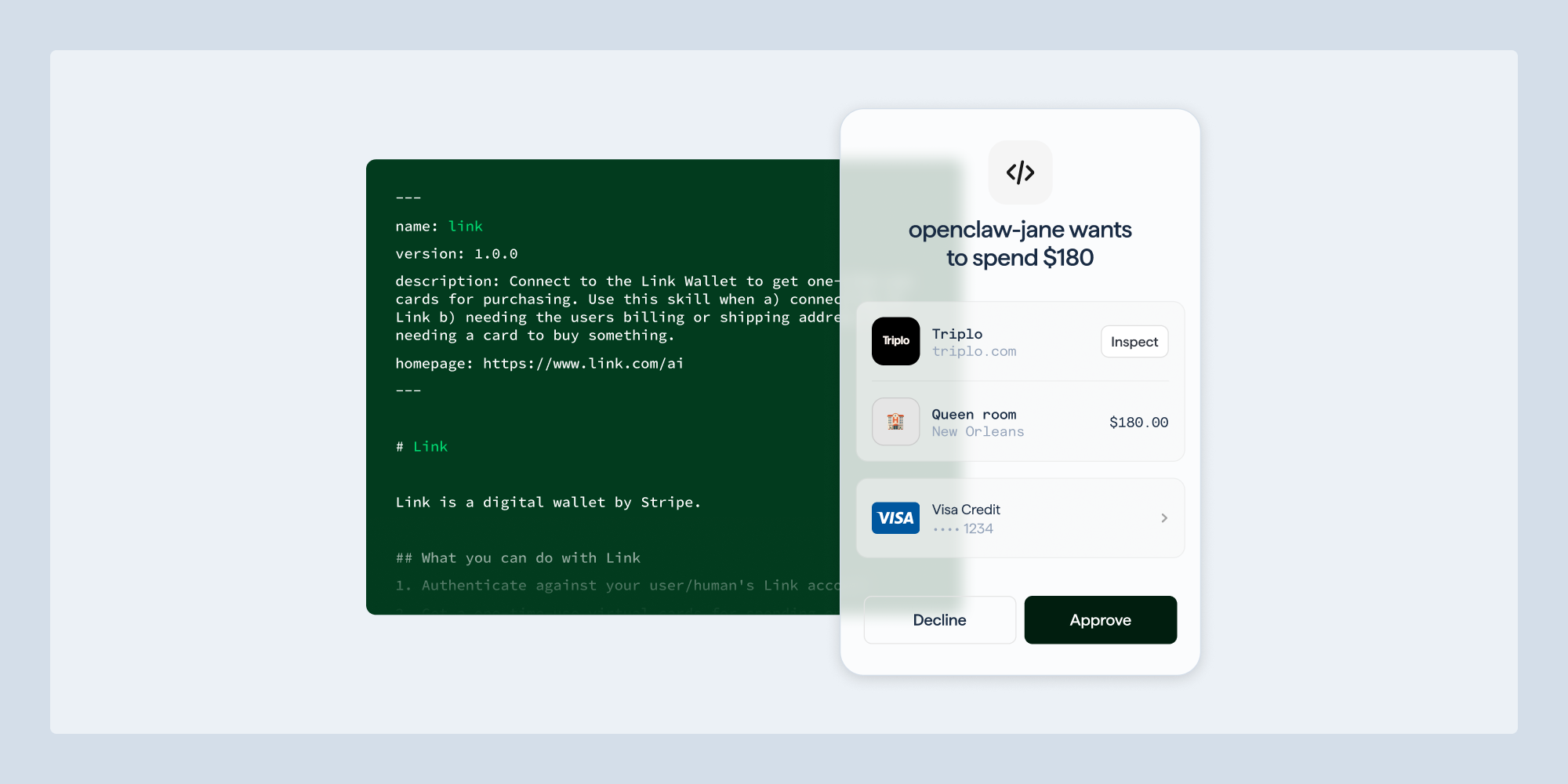

How it works is, predictably, a bit of a dance. Your consumer grants your agent access to their Link wallet, then the agent makes a ‘spend request.’ This request details the transaction, and you — the human overlord — get a notification to approve it. You can tweak this, of course, setting spending limits and deciding when your AI can act autonomously. After your digital nod of approval, the agent gets a one-time-use card or an SPT to complete the purchase. Your agent never sees your raw payment credentials. The whole shebang is managed through Link’s web and mobile apps. It’s designed to remove the burden of building wallet infrastructure from scratch for developers building consumer-facing agents. They can focus on the ‘AI magic,’ and Link will handle the payment plumbing.

Who’s Actually Making Money Here?

This is where my jaded journalist antenna starts twitching. Stripe, naturally, is selling the rails. Their Issuing API is getting an AI-flavored upgrade, allowing businesses to build custom agentic wallets and cards. Think about the implications for fintech providers, vertical SaaS platforms, and even marketplaces. They can embed this tech, issue cards under their own brand, automate supplier payments, manage expenses in real-time, and generally create new revenue streams by facilitating transactions. It’s a classic B2B play disguised as a consumer convenience.

Link, on the other hand, gets to tap into its existing user base of over 200 million consumers. By providing the wallet infrastructure, they position themselves as the central hub for these agent-driven transactions. They’re not just facilitating payments; they’re potentially building a new ecosystem where agent-to-agent or agent-to-business commerce becomes the norm. And who benefits directly? Developers building these agents, who now have a shortcut to enabling payment functionality. But let’s be clear, this isn’t charity. They’re enabling these developers to reach Link’s massive customer base, which is a powerful incentive.

What irks me is the PR spin. We’re talking about “agents as active participants in the internet economy.” It’s a lot of Silicon Valley jargon for ‘your AI can now buy you stuff.’ It’s reminiscent of the early days of e-commerce, where every new payment gateway or checkout optimization was hailed as a revolution. This is, arguably, just the next logical — albeit accelerated — step in that evolution.

The Underlying Infrastructure Play

Stripe’s involvement is key here. They’re not just enabling one company; they’re providing the generalized tooling for any business to create agent-powered financial workflows. This is a massive bet on the future of automation and programmatic commerce. If agents are going to be making decisions and executing tasks that involve money, then the underlying infrastructure needs to be incredibly secure, flexible, and scalable. Stripe Issuing for agents appears to be that infrastructure. They’re offering granular control over fund flows, spending limits, fraud prevention, and visibility into transactions. It’s a developer’s dream if you’re building in this space, and a potential cash cow for Stripe.

Consider the use cases outlined: automating business spend, embedding agent-issued cards for expense management, SMB customers using agents for automated spending under a platform’s brand, or marketplaces issuing cards to sellers for supply chain automation. These aren’t abstract future dreams; these are tangible business needs that companies are willing to pay for. Link and Stripe are simply offering a more efficient, AI-native way to address them.

Why This Matters for Developers (and Everyone Else)

The ability for agents to make payments means a whole new class of applications becomes feasible. Imagine agents that can autonomously manage your subscriptions, book travel based on your calendar and preferences without you lifting a finger, or even handle household replenishment of goods. The friction of payment has always been a bottleneck in full automation. By removing that bottleneck, Link and Stripe are essentially unlocking new levels of AI utility.

But with great power comes great responsibility — and of course, the potential for new kinds of fraud. While the article stresses that agents never get access to raw payment credentials, the reliance on approval workflows and scoped credentials still leaves room for error or exploitation. The speed at which these systems operate means that a compromised agent or a misconfigured approval could lead to significant unintended expenditures.

I’ve seen enough tech cycles to know that the initial rollout is just the beginning. What starts as a controlled, human-approved process will inevitably push towards greater autonomy for agents as the technology matures and trust (or at least, perceived trust) grows. This isn’t about ‘if’ your AI will be making purchases for you, but ‘when’ and ‘how much’ you’ll be comfortable letting it spend without your direct oversight. And that’s a conversation we should be having now, not after a few AI-driven shopping sprees go unexpectedly awry.

Today we’re launching Link’s wallet for agents, built on top of Stripe’s new Issuing for agents. You can now give agents programmatic access to Link and the ability to get a one-time-use card or a Shared Payment Token (SPT), backed by the cards and bank accounts already in your wallet.

This move by Link and Stripe is less about giving agents a ‘voice’ in the economy and more about giving them a wallet. It’s a pragmatic, infrastructure-level play that serves the businesses building AI solutions. The consumer convenience is the hook, but the real value is in the tools provided to developers and enterprises to monetize AI-driven transactions. It’s another chapter in the ongoing story of how technology intermediaries make the digital world, and the money within it, flow.

🧬 Related Insights

- Read more: [Alloy’s AI Bet] Spiekerman on Agentic AI vs Fraud

- Read more: [Wise Targets 8 Rails by 2026] Infrastructure Bet Analysis

Frequently Asked Questions

What does Link’s wallet for agents do?

Link’s wallet for agents allows developers to give AI agents programmatic access to make online purchases on behalf of users, using virtual payment methods tied to the user’s existing accounts without exposing sensitive card details. Users can review and approve these transactions.

Will this replace human oversight in spending?

Initially, the system requires user approval for each spend request. However, plans are in place to introduce more autonomous controls like spending limits, suggesting a future where human oversight may become less granular for approved agents.

Is this secure?

The system is designed with security in mind, using one-time-use cards and Shared Payment Tokens (SPTs) that do not expose raw payment credentials. However, as with any financial technology, potential risks related to agent compromise or misconfiguration exist, necessitating careful management of agent permissions.